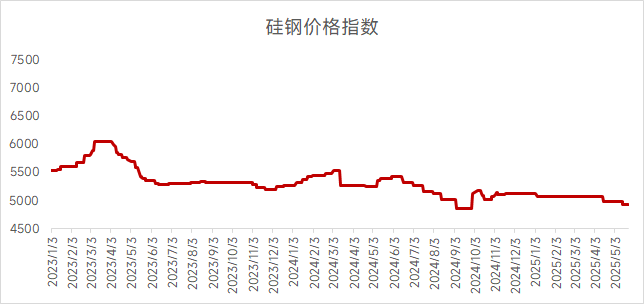

Price Dynamics of Non-Oriented Silicon Steel

Shanghai B50A800 Grade: 5,000-5,050 yuan/mt

Guangzhou B50A800 Grade: 4,750-4,850 yuan/mt

Wuhan 50WW800 Grade: 4,750-4,850 yuan/mt

Shanghai Market:

This week, the price of cold-rolled non-oriented silicon steel in Shanghai remained stable, with overall market transactions being average. The futures market for ferrous metals fluctuated rangebound, and the price of HRC fluctuated within a narrow range. The cost side saw relatively small changes, having a limited impact on the non-oriented silicon steel market. In terms of fundamentals, both state-owned and private producers have production lines entering the debugging phase, potentially leading to a further increase in the supply of non-oriented silicon steel. The spot liquidity of some grades was insufficient, and traders slightly lowered prices last week to facilitate sales. This week, the willingness to refuse to budge on prices was strong, but market transactions continued the weak trend from last week. The off-season effect gradually emerged, with end-user motor customers placing average orders, leading to cautious purchasing of raw material silicon steel and a heavy wait-and-see sentiment, with low restocking willingness. Looking ahead, the degree of supply looseness for non-oriented silicon steel may further expand, suppressing market confidence. However, steel mills have a strong willingness to refuse to budge on prices, coupled with active production cuts, making it difficult for prices to decline significantly in the future. In summary, the fundamental imbalance may continue to expand, but the imbalance has eased somewhat after the price adjustment. With steel mills refusing to budge on prices, the price of non-oriented silicon steel in Shanghai is expected to remain in the doldrums next week.

Wuhan Market:

This week, the spot price of cold-rolled non-oriented silicon steel in Wuhan remained stable, with average market transactions. The futures market for ferrous metals fluctuated within a narrow range, but the market trading atmosphere failed to recover. After last week's price adjustments, traders reported that sales were still poor. Fundamentally, Wuhan Iron and Steel's order intake was good, with overall inventory pressure being relatively small. The spot market had limited liquidity for some grades, but Wuhan Iron and Steel plans to add a new production line in June, which may alleviate the current shortage of spot resources. With the increase in supply, it will impact spot prices. Looking ahead, the market is gradually entering the off-season, with traders having a heavy wait-and-see sentiment and generally low inventory, leading to a situation where there are prices but no market. In summary, the price of non-oriented silicon steel in Wuhan is expected to adjust within a narrow range next week, but there is room for a long-term price decline.

Guangzhou Market:

This week, the price of cold-rolled non-oriented silicon steel in Guangzhou remained stable, with the spot market trading atmosphere remaining sluggish and showing no improvement. Fundamentally, the futures market for ferrous metals fluctuated rangebound, having no positive impact on the silicon steel market. However, traders maintained low inventory levels of non-oriented silicon steel, with relatively controllable sales pressure. Even though downstream end-user procurement demand remained weak and the pace of shipments was slow, traders were able to stabilize prices. Looking ahead, the market gradually entered the off-season, and demand was difficult to boost. Currently, the supply and demand for non-oriented silicon steel are both weak, barely stabilizing prices. In summary, it is expected that the price of non-oriented silicon steel in Guangzhou will remain stable next week.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)